New ‘Local File’ Requirements in Brazil

This article was first published by WTS Global Transfer Pricing Newsletter in July 2021.

Brazil is widely known for taking a different approach to transfer pricing rules, with Brazilian rules diverging substantially from the OECD Guidelines. This unique approach also extends to transfer pricing documentation requirements.

Out of the three standard documents recommended by the OECD as transfer pricing documentation requirements, Brazil has only effectively implemented the CbCR, in line with BEPS Action 13.

Brazilian taxpayers who are subject to transfer pricing rules are required to fill in certain registers of the Brazilian Electronic Tax Accounting bookkeeping (Escrituração Contábil Fiscal – “ECF”), which replaced the traditional corporate income tax return for calendar years 2014 and onwards. These specific registers are considered by some as a simplified Local File.

Although the portion relating to transfer pricing of the ECF is considered as a simplified obligation vis-à-vis the standards established under BEPS Action 13, the ECF is one of the most complex ancillary obligations annually submitted by Brazilian companies, containing detailed accounting information, the Corporate Income Tax calculation, information on Brazilian controlled foreign corporation rules, taxes paid abroad and information requested for Brazilian transfer pricing purposes, amongst others.

Every year, the Brazilian Federal Revenue Service updates the registers and entry fields contained in the ECF and, over the years, several new requirements were imposed to the taxpayer for the compliance with Brazilian transfer pricing rules. For FY 2020, the tax authorities included several additional entry fields in the ECF to be submitted, in principle, until the end of July 2021 (a deadline which will likely be extended due to the COVID-19 pandemic).

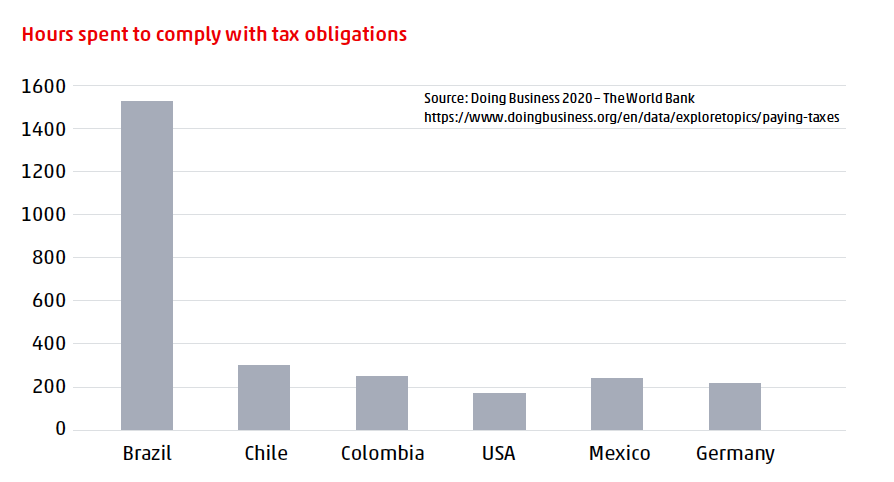

The increase in complexity of ancillary obligations is an everlasting concern for the Brazilian taxpayer, who already spends, on average, 1,500 hours to comply with the current ancillary obligations on an annual basis.

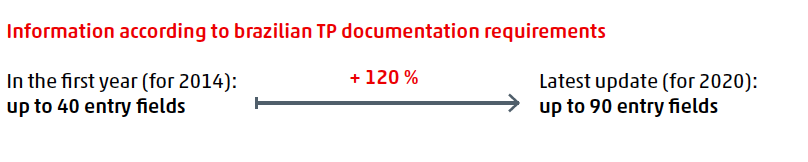

Specifically, in what refers to transfer pricing information requests in the ECF, a high-level comparison shows that the number of the entry fields required in the ECF have increased significantly over the years and, with the most recent inclusions, the increase was of almost 120% in comparison with the first year of existence of the ECF.

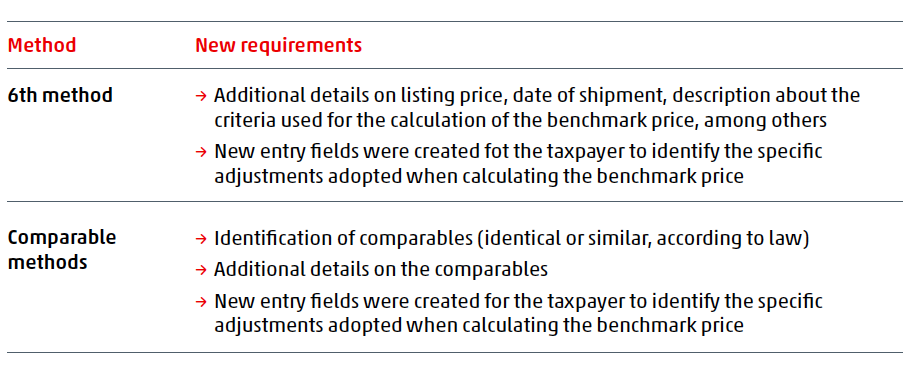

With respect to the new modifications included for FY 2020, it is important to note that the modifications will mainly affect the legal entities that use the 6th method (commodities) and/or the comparable methods to comply with transfer pricing rules.

This steady increase of the outflow of information regarding transactions subject to transfer pricing rules requires the taxpayer to be vigilant regarding compliance with the documentation requirements, especially considering that heavy fines may be imposed for submitting the ECF with missing or incorrect information.