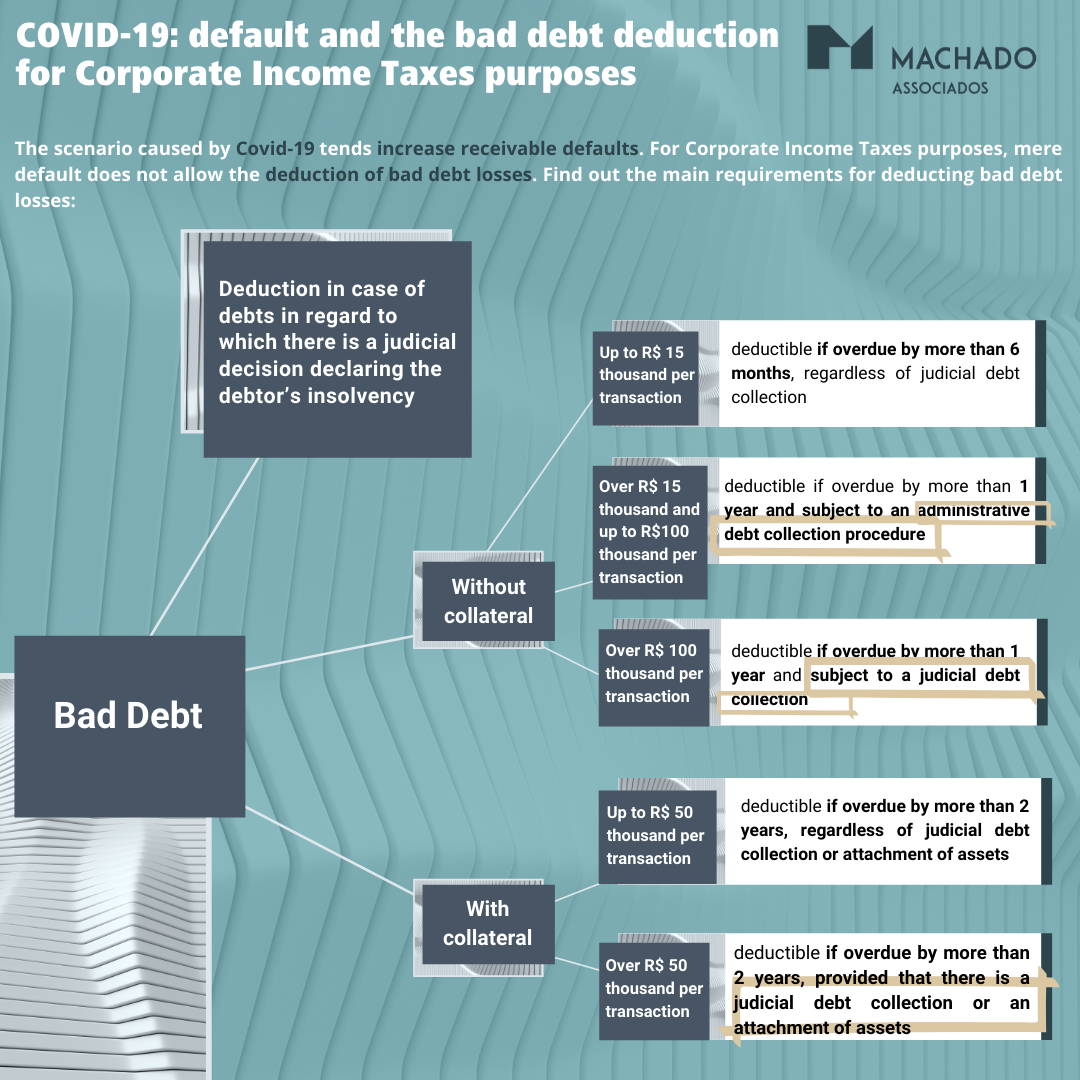

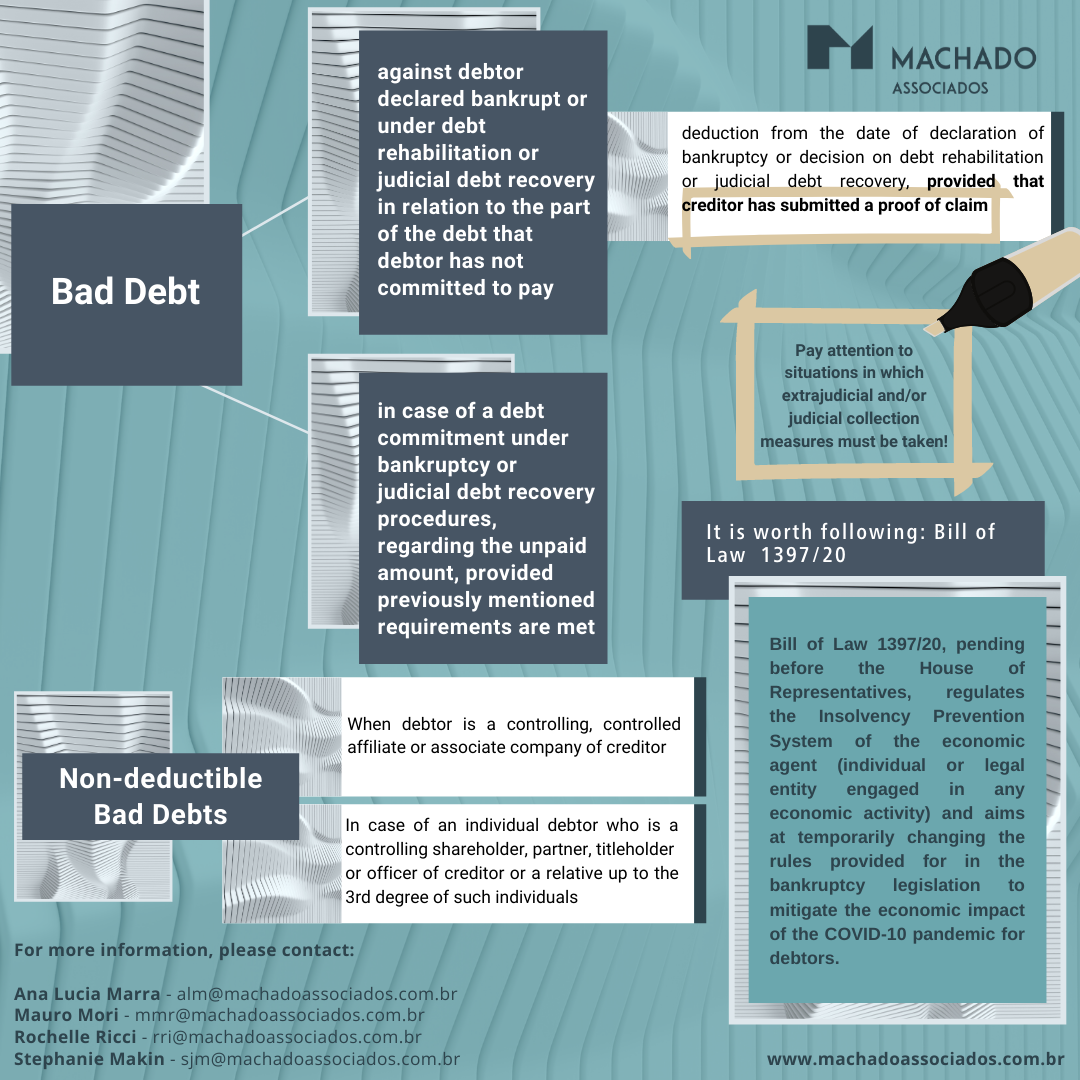

COVID-19: default and the bad debt deduction for Corporate Income Taxes purposes

The scenario caused by Covid-19 tends to increase receivable defaults. For Corporate Income Taxes purposes, mere default does not allow the deduction of bad debt losses. Find out the main requirements for deducting bad debt losses.